Estimating Project Costs

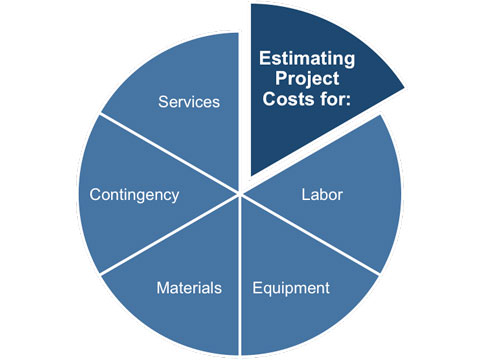

This step involves estimating the costs of all of the resources that will be charged to the project including: labor, equipment, materials, services, and any contingency costs.

|

In the early days of a project, estimating costs can be difficult particularly if there is little or no historical data from previous projects of a similar nature. There are various tools and techniques that can help with this but there is no substitute for experience. As the project progresses, more information becomes available and the degree of uncertainty naturally falls.

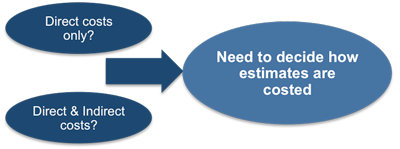

One basic assumption that needs to be made when estimating project costs is whether the estimates will be limited to direct project costs only or whether the estimates will also include indirect costs. Indirect costs are those costs that cannot be directly traced to a specific project and therefore will be accumulated and allocated equitably over multiple projects by some approved and documented accounting procedure.

|

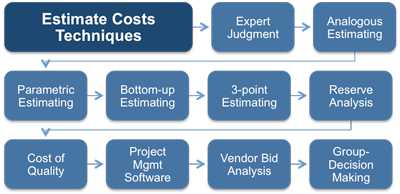

Cost estimates are influenced by numerous variables such as labor rates, material costs, inflation, risk factors, and other variables. Expert judgment, guided by historical information, provides valuable insight about the environment and information from prior similar projects. Expert judgment can also be used to determine whether to combine methods of estimating and how to reconcile differences between them.

|

Analogous Estimating

Analogous estimating uses the values of scope, cost, budget, and duration or measures of scale such as size, weight, and complexity, from a previous, similar project as the basis for estimating the same parameter for this project. It is most often used in the early stages of a project when there is little else to base the cost estimates on. It is a relatively quick and straightforward method but is less accurate than bottom-up estimation

The accuracy of the estimate depends upon how similar the activities are and whether the team member who will perform the activity has the same level of expertise and experience as the team member from the previous project.

Analogous estimating is typically a form of expert judgment that is most reliable when the previous activities are similar to the current activity and when the team members preparing the estimates have the necessary experience.

Parametric Estimating

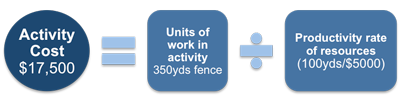

Another technique that can be used is parametric estimating, this is used to calculate the cost when the productivity rate of the resource performing the activity is available. You can use the following formula: Activity cost = Units of work in the activity / Productivity rate of the resources.

For example, if a contractor charges $5000 to build 100 yards of security fence, the cost calculation can be performed as follows:

|

This technique relies on the statistical relationship that exists between a series of historical data and the variables in question. When this data is being drawn from a large body of historical data taken from similar projects, then it can yield accurate estimates.

It provides several advantages as an estimating technique for example:

- It allows estimates to be prepared in much less time than required by more detailed techniques.

- It requires quantitative inputs that are linked to algorithms providing quantitative outputs. This means that all costs are traceable.

- If two estimators input the same values for parameters, they will get the same resulting cost. Parametric models also provide a consistent estimate format and estimate documentation.

- Parametric models provide costs for a range of input values, extrapolating to derive costs for projects of a different size or nature than you may have history for.

- The models highlight the design parameters used, and can provide key statistical relationships and metrics for comparison with other projects.

The disadvantages of this method are:

- Models will not exist for activities until there is a sufficiently large experience base for the activity. Basing estimates on work that is only vaguely comparable will yield inaccurate estimates.

- Physical parameters, for example 'number of bricks laid', 'area of trees cleared' or 'number of widgets produced' are far more meaningful than non-physical parameters for example, the 'number of lines of code' in a software project.

- Improved technology or working practices may make the historical data obsolete. As well as increased computing power this could include things like new plant and equipment or a completely new way of doing the job.

Three-point Estimating

Three-point Estimates address the issue of uncertainty in estimating the activity duration. This uncertainty can be calculated by making a three-point estimate in which each point corresponds to one of the following estimate types:

Most Likely Scenario (ML) - the activity duration is calculated in most practical terms by factoring in resources likely to be assigned, realistic expectations of the resources, dependencies, and interruptions.

Optimistic Scenario (O) - this is the best-case version of the situation described in the most likely scenario.

Pessimistic Scenario (P) - this is the worst-case version of the situation described in the most likely scenario.

We then find the average, but we first weight the Most Likely estimate by 4.

|

The formula is (O + (4*ML) + P) / 6. We must divide by six because we in effect have six different estimates (although three of these estimates are the same number). We are averaging (O + ML + ML + ML + ML + P) / 6.

Here's an example.

A roofing contractor is replacing all of the tiles on the roof of a house. He estimates that the job cost $10,000 based on the expectation that they will need to replace some of the underlying timbers. This is his Most Likely Estimate.

If none of the timbers need replacing then the job will cost $7,000, this represents his Optimistic estimate.

If most of the timbers need replacing then the job will cost $16,000, this represents his Pessimistic estimate.

Putting these numbers into the formula gives:

|

This formula is most useful in estimating the cost of activities for projects that are especially unique, such as in research and development where there are many unknowns.

Reserve Analysis

Cost estimates may include contingency reserves (sometimes called contingency allowances) to account for cost uncertainty. The contingency reserve may be a percentage of the estimated cost, a fixed number, or may be developed by using quantitative analysis methods.

One method of calculating the contingency reserve is to take a percentage of the original activity cost estimate, although it can also be estimated by using quantitative analysis methods. When more information about the project becomes available, the contingency reserve can be reduced or eliminated. Contingency should be clearly identified in cost documentation.

Cost estimating methods may include analysis of what the project should cost, based on the responsive bids from qualified vendors. Where projects are awarded to a vendor under competitive processes, additional cost estimating work can be required of the project team to examine the price of individual deliverables and to derive a cost that supports the final total project cost.

|

Activity Cost Estimates are quantitative assessments of the probable costs required to complete project work. They are estimated for all resources that are applied to the activity cost estimate including, direct labor, materials, equipment, services, facilities, information technology, and special categories such as an inflation allowance or a cost contingency reserve. They should also provide a clear and complete understanding of how the cost estimate was derived including: the basis of the estimate, all assumptions made, any known constraints, indication of the range of possible estimates, and the confidence level of the final estimate.

You may also be interested in:

Managing Project Costs | Estimating Project Costs | Calculating the Total Project Budget | Monitoring Project Expenditure | Buying-in Goods and Services | Managing Project Suppliers | Planning Contract Management | Understanding Different Contract Options | Managing Supplier Relationships.

|

|