Managing Project Costs

Managing project costs involves defining the total cost of the project, securing a budget and then making sure that it is delivered within that approved budget. It relies on other planning processes like scope management and resource allocation being done effectively.

The first step in managing project costs is to answer the questions: 'How much will the project cost?' and 'How accurate is this estimate?'

Project managers make many of their day-to-day decisions based on estimates and the accuracy of these can have a big influence on the outcome of the project. Experience suggests that projects launched without an accurate initial estimate are far more likely to experience serious problems than those where sound estimates were made. One of the keys to successful project completion is an accurate cost estimate and a realistic risk assessment.

|

In addition, in some project environments, the project manager may have a legal responsibility for ensuring that cost estimates are prepared properly. Even where this is not the case the project manager should document all of the supporting information that went into the cost estimates in order to justify their decisions if these are challenged later on.

In common with many of the processes in project management, cost estimation is an iterative process and the more work that is done and the more experience that is gained the more accurate the estimates of future work will become.

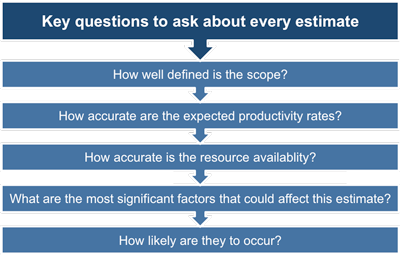

Even projects with acceptable initial estimates are doomed to overrun cost and schedule budgets if they are not guided by rules of thumb and rigorous estimates-to-complete. There are five questions project managers should ask about every estimate as they define and manage their projects:

1. How well defined is the scope?

2. How accurate are the expected productivity rates?

3. How accurate is the resource availability assumption?

4. What are the most significant factors that could affect this estimate?

5. How likely are they to occur?

|

There is no point in working out costs to the nearest dollar if you are not clear about these things. In fact, providing very specific cost estimates to the sponsor can hide the fact that you are basing them on scope, resource and productivity figures that are themselves likely to be revised in the light of experience.

On the subject of accuracy, you will need to decide just how accurate the estimates need to be. For example, an initial estimate may suggest a figure of between $50,000 and $75,000 for a particular part of the project. The benefit gained from narrowing this down needs to be factored against the additional time (and cost) it would take to do so. If the project sponsor is happy to accept this initial estimate, then why bother? The key word here is 'initial', you should be able to narrow this down without too much effort when you have more experience and more data to work with.

Whilst cost estimating operates at the level of activities, cost budgeting aggregates these figures at the project level to produce a cost baseline and the project funding requirements. The process of aggregation involves more than simply adding the figures from the estimating process to produce totals.

|

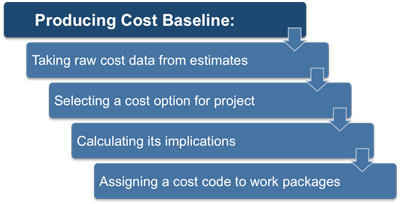

Budgeting involves taking the raw cost data from the estimating step, deciding which cost options to use, calculating their implication, and finally assigning cost codes to work packages. The project cost plan will also need to be structured in a way that is compatible with how the funds are being disbursed and it will need to be compatible with the organization's own accounting system.

Cost control is concerned with answering the questions:

1) Is the project on track in terms of cost to date?

2) Does it look as if this will continue?

3) If not, what action can be taken to remedy the situation?

|

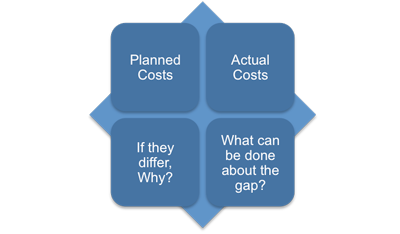

To answer these, you need to know four things:

1) The planned costs

2) The actual costs

3) Why they differ (assuming they do)

4) What you can do about it

The process of determining the difference between the planned costs and the actual costs is fairly straightforward and there are several tools that can be used to quantify any 'variance'. A project manager is expected to be able to report exactly where a project is in terms of costs against the planned budget. You will normally be expected to produce a variance report to the project sponsor detailing these figures.

The real skill of project management is to be able to identify problems and to address them as soon as possible, before they become too big to fix.

The cost plan clearly defines how the costs on a project will be managed throughout the project's lifecycle. It sets the format and standards by which the project costs are measured, reported and controlled. This plan identifies who is responsible for managing costs and who has the authority to approve changes to the project or its budget. It also specifies how cost performance is quantitatively measured and details report formats, frequency and to whom they are presented.

The work breakdown structure (WBS) is the basis for the cost plan because the costs are totaled or "rolled up" from the costs for the individual work packages in the WBS. You can check out the complete range of project management pdf eBooks free from this website.

Developing the cost plan may involve choosing strategic options to fund the project such as:

• Self-funding,

• Funding with equity, or

• Funding with debt.

The cost plan may also detail ways to finance project resources such as making, purchasing, renting, or leasing. These decisions, like other financial decisions affecting the project, may affect project schedule and/or risks.

|

Organizational policies and procedures may influence which financial techniques are employed in these decisions. Techniques may include (but are not limited to): payback period, return on investment, internal rate of return, discounted cash flow, and net present value.

You may also be interested in:

Managing Project Costs | Estimating Project Costs | Calculating the Total Project Budget | Monitoring Project Expenditure | Buying-in Goods and Services | Managing Project Suppliers | Planning Contract Management | Understanding Different Contract Options | Managing Supplier Relationships.

|

|