Monitoring and Controlling Project Expenditure

This is the process of monitoring the status of the project to update the project budget and managing changes to the cost baseline. It involves taking the cost baseline and performance data about what has actually been done in order to determine the work accomplished against the amount spent.

Monitoring the expenditure of funds without regard to the value of work being accomplished for such expenditures has little value to the project other than to allow the project team to stay within the authorized funding. The key to effective cost control is the management of the approved cost performance baseline and the changes to that baseline.

For those projects that are funded at various stages during the project, funding requirements will need to be taken into account so that the project doesn't get to the point that funding is temporarily unavailable.

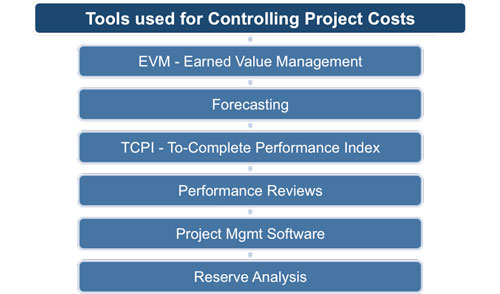

Earned value management (EVM), forecasting, the TCPI (To-Complete Performance Index), and performance reviews are the main techniques used, along with the project management software. Earned value management takes a snapshot of the present moment to see how the project is doing.

The techniques of forecasting and TCPI shows how the future of the project will evolve given how the project is doing now. The performance reviews compare the past performance with the present performance to see how the project has evolved up until the present moment.

|

Reserve analysis takes into account the 'extra layers' on top of the cost estimates, the contingency reserves (which are added to the cost estimates to get the cost baseline) and the management reserves (which are added to the cost baseline to get the project budget). It should be decided whether any unused reserves are going to be left in the project budget, or whether they will be taken out.

Not every organization uses EVM and even if yours does not, it is still worth taking the time to understand it because it can help you to determine for yourself how a project is progressing in circumstances where you need to provide objective figures to your senior management or other stakeholders.

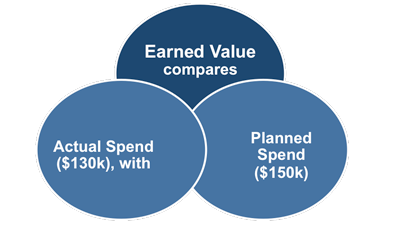

The rationale behind this method is to compare the planned cost data with the actual costs and independently with the progress made. It works like this:

• Planned costs to date were $150k

• ONLY $130 had actually been spent.

This could indicate that the project was under budget BUT only if all of the planned work has actually been completed. EVM introduces a third-dimension by taking account of the percentage of the work accomplished.

In the example,

• Project Total budget is $350

• Project is reported 40% complete

• Notional value of the project would be $350 x 0.4 = $140

|

The earned value compares the money spent ($130k) with what should have been spent ($150k). This means that:

• Work to the notional value of $140k has been done but,

• $130k has actually been spent.

• Therefore, the project is $10k under its planned cost at this point.

Also the project has only completed $140k of work as opposed to the $150k that was planned.

This means that the project is $10k behind schedule.

It may seem strange to express time in dollars but the reason it makes sense is because 'time is money'.

|

As the project progresses, the project team can develop a forecast for the estimate at completion that may differ from the budget at completion based on the project performance. Earned Value Management method works well in conjunction with manual forecasts of the required estimate at completion costs. The most common approach is a manual, bottom-up summation by the project manager and project team.

If either the work performance information or the cost forecasts indicate that there is a variance in either the cost or schedule performance of the project that needs correcting, then a change request may be recommended.

1) Corrective action aims to reduce the variance

2) Preventive action aims to prevent the variance from growing larger in the future.

It may happen, however, that the variance is so large that the cost baseline is determined to be unrealistic, in which case it may be suggested that the cost baseline itself is changed.

You may also be interested in:

Managing Project Costs | Estimating Project Costs | Calculating the Total Project Budget | Monitoring Project Expenditure | Buying-in Goods and Services | Managing Project Suppliers | Planning Contract Management | Understanding Different Contract Options | Managing Supplier Relationships.

|

|