Accounting Concepts - Revenue Recognition Principle

Organizations all have primary activities and it is the revenue or incomes generated by these activities that are referred to as 'sales' or 'sales revenue.' For example, a retailer will buy goods, which they then sell on. It is the sale of these products that creates their revenue. This Accounting Terminology Checklist outlines the terminology, concepts and conventions that are accepted within the accounting profession.

For service organizations the primary activities are the acquisition of and selling of skills and expertise. These revenues are often referred to as fees earned, income, or service revenues.

|

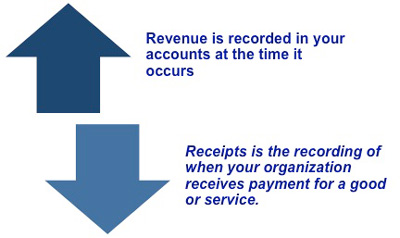

Under accrual accounting, revenues are reported as they occur - that is 'when they are recognized' - and not when the payment is received. For instance, your organization sells its service to a customer for $5,000 in December, offering them 60 days to pay. Your accounts would show a revenue figure of this amount in December.

When at the end of February the invoice is paid your accounts would show a receipt of cash for that amount. It would also show a reduction in your accounts receivable (some organizations refer to this as 'collection'). It is important to appreciate the distinction between receipts and revenues so that the latter are only recorded once when the primary activity has been performed.

You also need to appreciate how the following will be represented in your organization's accounts:

• When a pre-payment or deposit is taken

• When payment is made in cash

• When funds are received in the form of a loan (e.g. from a bank)

Where your organization requests a payment (or deposit) for a service or product in advance of any work being performed this is known as a 'receipt.' Only once the customer's work begins will it be shown in your accounts as a 'revenue' item. For example:

Your organization sells a product for $800 in May and requests a $200 partial payment at the time of sale, prior to delivery in June. This $200 appears in your accounts as a liability in May and only when the product has been delivered to the client will the accounts show $800 revenue.

In circumstances where organizations are concerned about a customer's ability to pay or their creditworthiness a deposit can be requested prior to the work starting. This deposit would be recorded in the same way as a pre-payment in your accounts, i.e. as a receipt.

In the event that your organization receives cash in direct exchange for its product or service this will be recorded in the accounts as both a 'receipt' and 'revenue.' This is because it has been given the cash 'receipt' on the same day the actual service or product (the 'revenue') occurred. For example:

A dealership sells a car on April 23 for $650 cash. This sale would be represented in the dealer's accounts as both a 'receipt of $650' and 'revenue of $650' on that date.

In a situation where your organization needs to extend its mortgage or seeks a short-term loan, such funds are shown in your accounts as a 'receipt' and referred to as a current liability.

There would not be 'revenue' for this amount within your accounts because no goods or services have been exchanged or performed. For example:

The $12,500 extension to your organization's overdraft would be shown in your accounts only as a 'receipt' of $12,500 on the date such funds became available. It cannot be recorded as 'revenue' because it was not earned as a result of delivering a product a service.

You may also be interested in:

Accounting Concepts and Conventions | Basic Accounting Concepts and Financial Statements | Cash Accounting | Accrual Accounting | Basic Accounting Terms | Revenue Recognition Principle | Matching Principle | Example Income Statement.

|

|

|